Diego Franzin, Head of Portfolio Strategies, Plenisfer Investments SGR

For decades, the Defence sector was treated by financial markets as a cyclical sector with unique characteristics: concentrated government orders, high entry barriers, multi-year cycles linked to geopolitical tensions. It was viewed as a tactical rather than a structural investment—something to overweight when the radar lights up and to reduce when tensions ease.

This outlook is becoming obsolete. Not so much because geopolitics has changed—although it has, profoundly—but because the very nature of Defence has changed. What we are witnessing is not an acceleration of the traditional rearmament cycle. It is a reorganization of public and private spending around a new economic category: physical and digital security.

The distinction is crucial. A cycle reverses. An infrastructure is accumulated.

The New Scope of Defence

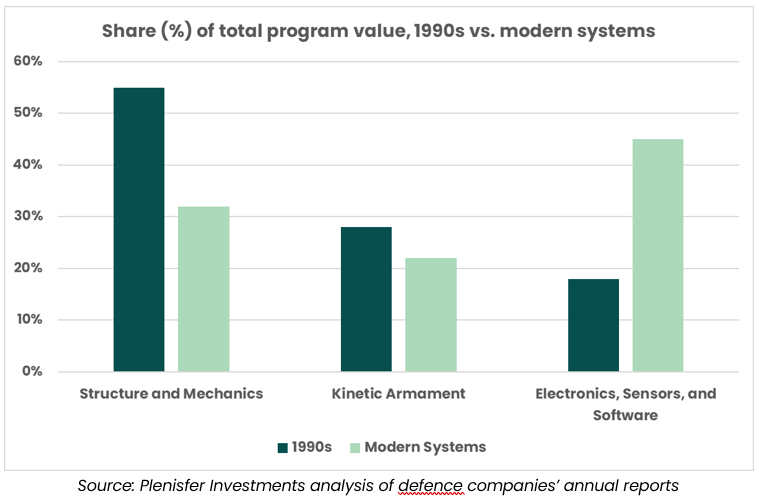

The transformation is visible in the structure of military programs. In the 1990s, the electronics, software, and sensors component represented less than 20% of the total value of an advanced system[1]. Today, in next-generation systems, that share stands between 35% and 45%[2], while the mechanical part has decreased from more than half of the value to just over a third[3].

This is not a marginal technical evolution. It is an industrial paradigm shift. An industry that, for two centuries, sold physical platforms—tanks, ships, airplanes—has transformed into an industry that sells integrated information collection and processing systems with embedded physical capabilities.

The economic difference is substantial: discrete capex vs. recurring revenue, depreciation vs. continuous updates, consumption vs. value increase over time.

This logic is already visible in industrial strategies. For example: Rheinmetall, a historic European producer of munitions and armored vehicles with a backlog of over 60 billion euros, aims to generate between 8 and 10 billion in digital revenues by 2030—potentially about a third of the total—with expected operating margins between 17% and 19%[4], higher than its traditional business. Indra Sistemas, the Spanish leader in radar and Air Traffic Management (ATM) systems, with an order portfolio of about 9.5 billion euros, aims to reach 10 billion in revenues by 2030, with margins above 14%[5], driven by high-tech activities.

The Macro Context: From Threshold to Mandate

This industrial change is part of a structural transformation of spending.

Global military spending is projected to grow by about 900 billion dollars, surpassing 3.6 trillion by 2030 and bringing the weight on global GDP towards 3%[6]. But the aggregate number tells only part of the story.

The most significant change is qualitative: the shift from a minimum threshold logic to a structural mandate logic. At the 2025 NATO Summit in The Hague, the allies adopted a new two-level framework: at least 3.5% of GDP for traditional Defence, plus up to 1.5% for critical infrastructure, digital network security, civil readiness, and innovation, for a potential total of 5% by 2035[7].

It is this second component that represents the deepest discontinuity. It does not finance military platforms but the operational continuity of the economic system: power grids, digital infrastructure, submarine cables, industrial capacity.

In 2025, for the first time, all European allies exceeded the 2% of GDP threshold, with an overall spending increase of about 20% year over year[8]. The signal is that the transition is no longer just declarative.

Digital and military security are no longer separate domains. They become two manifestations of the same function.

Artificial Intelligence: From Operational Capability to Systemic Function

In this context, the role of artificial intelligence is evolving. The debate has long focused on its contribution to productivity—including in the military—or associated risks. Both perspectives are partial. The most significant novelty is that AI is assuming a systemic function: identifying, diagnosing, and correcting potential vulnerabilities in complex digital systems, not just in the traditional Defence sector.

A concrete example is Claude Mythos, the model developed by Anthropic as part of Project Glasswing. Nicholas Carlini, one of the world's most respected cybersecurity researchers, summed up its impact with a clear statement: "I’ve found more bugs in the last few weeks than in the rest of my career combined."

This capability introduces a logic of continuous maintenance that redefines the very perimeter of Defence. Protection no longer means only deploying military platforms: it means ensuring the operational continuity of power grids, payment systems, communication infrastructures, submarine cables. The line that once separated military Defence and civilian infrastructure security has become so thin as to be irrelevant. In the modern world, vulnerability is systemic and does not distinguish between physical and digital, military and civilian.

The Pentagon has already structurally incorporated this approach. For fiscal year 2026, the Department of Defence allocated a total of 179 billion dollars for Research, Development, Testing, and Evaluation (RDT&E)[9]— a 27% increase over the previous year. For the first time in American budget history, there is a line dedicated exclusively to autonomous systems and artificial intelligence, amounting to 13.4 billion dollars[10]. AI in Defence is no longer experimental; it has become a permanent category in the federal budget.

The global market for AI applied to Defence reflects this trajectory: according to the latest estimates, it is projected to grow from about 8.5 billion dollars in 2026 to over 32 billion in 2031, with a compound annual growth rate of nearly 30%[11]. This figure likely underestimates the true size of the phenomenon, as it does not capture defensive cybersecurity spending distributed among civilian and infrastructure budgets, nor the funds classified in NATO's additional 1.5% framework for network and critical infrastructure protection.

Operational Evidence: Ukraine and Cost Asymmetry

This transformation is empirically validated by recent conflicts. The war in Ukraine has clearly shown that the relationship between cost and operational capability has changed. Autonomous systems costing just a few hundred dollars can neutralize traditional platforms worth 3–5 million dollars. Not as an exception, but as the operational norm. This asymmetry reorganizes investment priorities.

Platforms remain relevant, but value shifts toward distributed, upgradable, and integrated systems. Autonomous drones, operational even in highly jammed environments and without GPS dependence, have gone from prototypes to large-scale production in a matter of months. At the same time, the market for countermeasures against these technologies is rapidly growing: the counter-UAS segment—systems for detecting and neutralizing enemy drones—is estimated at 6.6 billion dollars in 2025 and projected to exceed 20 billion by 2030, with a compound annual growth rate of 25%[12].

The point is not any single innovation, but the speed at which it is validated and scaled.

Who Captures the Value: The Supply Chain Map

If Defence takes on infrastructure characteristics, the question is no longer how much will be spent, but where that spending will result in lasting value.

Value tends to concentrate where technical complexity, certification requirements, and operational integration create dependencies that are difficult to remove. Critical hardware is the first level: multi-year programs, high standards, and constrained supply chains reduce cyclicality and increase revenue predictability. The next step is integration. When data, AI, and operational processes are incorporated into a specific architecture, the replacement cost rises and the revenue model begins to resemble that of digital infrastructure. Finally, sovereign platforms emerge: management of classified data, isolated environments, certified security. Here is where the convergence between military Defence and digital security is most apparent.

This transformation has direct implications for how the market attributes value.

Traditional Defence activities still tend to reflect a cyclical logic, with compressed multiples and limited visibility. By contrast, components more exposed to software, integration, and data management are beginning to show features typical of infrastructure: recurring revenues, greater stability, and over time, higher and more sustainable multiples.

This is the point of misalignment. The market still partly prices Defence as a cycle, while a growing share of the sector behaves as infrastructure.

The underlying theme is simple: Defence is no longer a cycle but a permanent cost structure.

When security becomes a necessary condition for the functioning of the economy, the associated spending ceases to be compressible. And when spending becomes structural, value concentrates in nodes that are difficult to disrupt.

For an investor, the relevant distinction is not between Defence and non-Defence, but between exposure to recurring revenues and dependence on discretionary cycles.

That’s where the structural revaluation of the sector is playing out.

[1] Plenisfer Investments analysis of defence companies’ annual reports

[2] Plenisfer Investments analysis of defence companies’ annual reports

[3] Plenisfer Investments analysis of defence companies’ annual reports

[4] Rheinmetall AG - Investor Presentation (3 March 2026)

[5] Indra Sistemas - Investor Presentation (30 October 2024)

[6] Plenisfer Investments analysis of NATO data

[7] Nato, The Hague Summit Declaration (25 June 2025)

[8] Plenisfer Investments analysis of SIPRI data

[9] U.S. Department of Defense, FY2026 Budget Request Overview, June 2025

[10] U.S. Department of Defense, FY2026 Budget Request, June 2025

[11] Knowledge Sourcing Intelligence, AI in Defense Market: Forecast 2031, 2025, knowledge-sourcing.com

[12] MarketsandMarkets, Counter-Unmanned Aircraft System (C-UAS) Market - Global Forecast to 2030, October 2025

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and does not constitute a marketing communication relating to a fund, an investment product or investment services in your country. This document does not constitute an offer or invitation to sell or purchase securities or any assets or businesses described herein and does not form the basis of any contract. Any opinions or forecasts provided are as of the specified date, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance is not indicative of future returns. There can be no guarantee that any investment objective will be achieved or that capital will be returned. This analysis is intended exclusively for professional investors in Italy pursuant to Directive 2014/65/EU on markets in financial instruments (MiFID). It is not intended for retail investors or U.S. Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended. Information is provided by Plenisfer Investments, authorised as a UCITS management company in Italy and regulated by the Bank of Italy – Via Niccolò Machiavelli 4, Trieste, 34132, Italy – CM: 15404 – LEI: 984500E9CB9BBCE3E272. All data used in this analysis, unless otherwise stated, are provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.