Marco Mencini, Head of Research, Plenisfer Investments SGR

Four years after Russia’s invasion of Ukraine, a new conflict has brought energy back to the center of the global economic system in a way that the market had gradually forgotten. Energy is no longer a cyclical variable, but a structural constraint capable of simultaneously influencing inflation, growth, geopolitical balances, and technological trajectories.

The escalation of the conflict in Iran currently represents the most visible manifestation of this shift, though it is not its root cause. Rather, it acts as a catalyst, bringing to light a fragility that was already embedded in the system.

For over a decade, markets operated under the implicit assumption that energy was abundant and readily accessible. The expansion of U.S. shale production, combined with relatively stable demand and the rise of the ESG paradigm, contributed to the marginalization of the traditional energy sector within global asset allocation. Energy became a low-growth segment, underrepresented in equity indices, accounting today for only 3–4%[1], compared with approximately 14–15%[2] of the S&P 500 in the early 1990s, when the First Gulf War broke out.

Yet once again, indices reflect a backward-looking snapshot rather than current dynamics and forward-looking trends in a sector that, under the pressure of geopolitical tensions, structural increases in demand, and supply constraints, is now more strategic than ever.

From Abundance to Energy Security

The first key shift concerns the distinction between abundance and availability. Global energy resources remain vast, but their geographic distribution and the reliability of production areas are becoming decisive factors. Not all resources are equal: as the political context changes, so does the stability of infrastructure and the predictability of supplies.

The conflict in Iran fits precisely within this framework. It is not merely a direct supply risk, but a factor that increases the risk premium across an entire region that is strategic for global energy markets. Even in the absence of immediate supply disruptions, heightened uncertainty alone can materially impact prices, logistics, and investment decisions. Russia, Iran, and Venezuela collectively account for more than 10 million[3] barrels per day of seaborne exports—a meaningful share of global supply (over 10%) exposed to geopolitical risk.

The Middle East is emblematic because it combines high resource availability with high geopolitical risk. However, the same principle applies to other emerging regions: energy availability is no longer sufficient unless accompanied by political stability and adequate infrastructure. Markets are therefore progressively pricing not only extraction costs but also the geopolitical reliability of supply.

This vulnerability arises in a context already weakened by years of underinvestment. Regulatory pressures, decarbonization policies, and a widespread perception of a “sunset cycle” for traditional energy sources have significantly reduced capital flows into the sector. The result has been a gradual erosion of both productive capacity and the underlying industrial base.

A More Rigid System in a More Unstable World

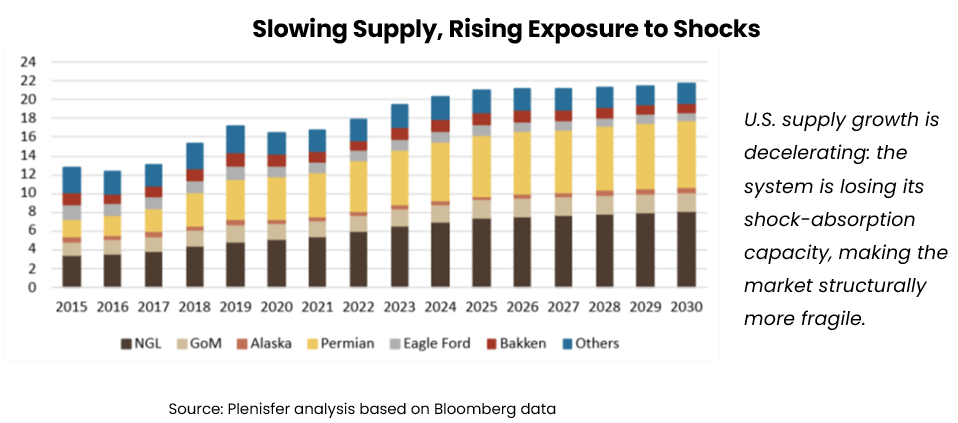

At the same time, some of the main drivers of supply growth are showing signs of fatigue. The U.S. shale cycle, arguably the most important source of supply expansion over the past fifteen years, is entering a more mature phase. Production reached approximately 13.6 million barrels per day in 2025, with a peak expected around 13.8 million[4], indicating a clear deceleration in growth.

This marks a significant shift: the system is losing its main “buffer.” In the past, U.S. shale acted as a balancing mechanism: higher prices would quickly trigger increased production, offsetting global supply disruptions. Today, that responsiveness is more limited. Greater capital discipline, sector consolidation, and basin maturity are slowing the pace at which output can expand, reducing supply elasticity precisely when tensions rise.

The overall result is an increasingly rigid energy market. Supply is less elastic, spare capacity is shrinking, and a growing share of production is exposed to geopolitical risk. While the market appears to be in surplus (around 1.8 million barrels[5] per day), this balance is supported by a few temporary factors, making it more vulnerable to sudden shocks. The system is no longer designed to absorb volatility but tends to react in a non-linear manner.

This fragile equilibrium is increasingly supported by demand dynamics, particularly through China’s role. In recent years, Beijing has accumulated record levels of oil inventories, exceeding 1.2 billion barrels, equivalent to more than 100 days of imports[6].

This stockbuilding process has effectively acted as a market buffer, absorbing part of the excess supply and helping stabilize prices. In a context of growing uncertainty over supply reliability, strategic inventory management becomes a central pillar of global equilibrium, reinforcing the stabilizing role of demand.

Overlaying this dynamic is a second structural factor: the emergence of artificial intelligence as a driver of energy demand. The expansion of data centers and digital infrastructure is fundamentally reshaping consumption patterns, introducing demand that is continuous, concentrated, and relatively inflexible. This type of demand requires stable and dispatchable energy, exposing the limitations of systems predominantly reliant on intermittent sources.

This creates an inherent tension between energy transition and security of supply. In recent years, policy and market focus has been centered on decarbonization as a primary objective. Today, the need to balance this goal with system stability is becoming increasingly evident. The transition cannot be linear, as it must contend with physical and industrial constraints.

An additional layer of complexity arises from the growing geographical divergence in energy prices. While oil remains a globally priced commodity, natural gas markets have become increasingly regionalized. As a result, economic competitiveness is now influenced not only by technological and financial factors but also by relative energy costs.

In this context, Europe appears particularly vulnerable. The combination of import dependence, regulatory constraints, and delayed investment reduces the system’s adaptability. At the same time, rising demand linked to new technologies risk further widening this gap. This is not merely an economic issue but a strategic one, directly affecting the region’s ability to sustain long-term industrial development.

The return of energy security therefore represents the true paradigm shift. The objective is no longer simply cost optimization, but ensuring long-term access, stability, and predictability. This implies a renewed emphasis on industrial policy and strategic planning, with resilience increasingly prioritized over efficiency.

From an investment perspective, these dynamics suggest that the energy sector is entering a new phase of the cycle. The combination of constrained supply, rising demand, and limited capacity creates conditions for structurally improved profitability. In particular, capacity constraints and reduced competition are strengthening pricing power across the value chain.

Generally speaking, energy is once again emerging as a core real asset within a macro environment characterized by more persistent inflation and heightened uncertainty. In this sense, the conflict in Iran should not be viewed as an isolated event, but as a sign of a deeper shift: the transition into a phase where energy availability becomes one of the primary drivers of global growth.

[1] Source: Plenisfer analysis based on Datatrek Research data

[2] Source: Plenisfer analysis based on SSGA data

[3] Source: Plenisfer analysis based on World Bank data

[4] Source: Plenisfer analysis based on Bloomberg data

[5] Source: Bloomberg

[6] Source: OPEC

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and does not constitute a marketing communication relating to a fund, an investment product or investment services in your country. This document does not constitute an offer or invitation to sell or purchase securities or any assets or businesses described herein and does not form the basis of any contract. Any opinions or forecasts provided are as of the specified date, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance is not indicative of future returns. There can be no guarantee that any investment objective will be achieved or that capital will be returned. This analysis is intended exclusively for professional investors in Italy pursuant to Directive 2014/65/EU on markets in financial instruments (MiFID). It is not intended for retail investors or U.S. Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended. Information is provided by Plenisfer Investments, authorised as a UCITS management company in Italy and regulated by the Bank of Italy – Via Niccolò Machiavelli 4, Trieste, 34132, Italy – CM: 15404 – LEI: 984500E9CB9BBCE3E272. All data used in this analysis, unless otherwise stated, are provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.