Diego Franzin, Head of Portfolio Strategies, Plenisfer Investments SGR

In January, gold traded near the all-time high of $2,030 per ounce, after already recording a 15% increase in value in 2023.

To assess the potential prospects of gold, it is necessary to make a premise and identify the factors that could support or undermine its value over time.

Firstly, the premise: if the price of gold is adjusted for inflation to make it comparable to past values, it emerges that the peak reached by gold is only apparent and still far from the values (normalized for inflation) reached during previous peaks, namely: around $2,500 in the late 1970s - during the oil crisis - between 2011 and 2014 - during the sovereign debt crises - and more recently, during the pandemic phase, at around $2,350.

Source: Plenisfer, Bloomberg

As for the factors, at Plenisfer we believe there are at least three: 'uncertainty,' central banks' demand, and financial flows. These three factors have impacted the value of gold in 2023 and, in our opinion, should be carefully monitored in the years to come.

The year 2023 was dominated by 'uncertainty', on the one hand due to the development of inflation and, consequently, the actions of monetary policy, and on the other hand, the rising geopolitical tensions. Not to mention the uncertainties related to the record levels reached by sovereign debts. In phases of uncertainty, gold traditionally fulfils its role as a safe-haven asset, and the resulting purchases support its price.

However, what primarily supported the price of gold in 2023 was a second factor: the robust demand from central banks. Gold plays a significant role in their global reserves. After the outbreak of the 2008 financial crisis, we witnessed a fundamental shift, with central banks progressively reevaluating the role and relevance of gold in reserves. Specifically, central banks in emerging markets increased their gold purchases, U.S. central banks maintained constant reserves, while European central banks ceased selling. In the third quarter of 2023 alone, central banks collectively purchased 337 thousand tons of gold, the second highest ever recorded for a third quarter, bringing net annual purchases to the astonishing amount of 800 thousand tons, a 14% increase from 2022 (source: Bloomberg).

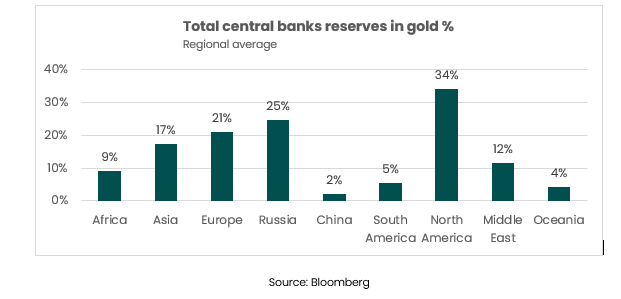

At Plenisfer, we expect this trend to continue, especially supported by Emerging Countries grappling with a de-dollarization process, particularly in Asia. Consider that central banks' gold reserves account for 34% of the total in North America - the highest level ever - compared to China's 2% or South America's 5% (source: Bloomberg). While we do not expect it to lead to a regime change on the dollar as the international reference currency, it could result in gold having a greater impact on reserves compared to the amount of dollars held by central banks.

This factor could, in our view, further support gold purchases and thus its value.

The third factor to monitor in gold is the one related to financial flows. Gold still does not seem to appeal to investors in ETFs.

2023 marked the third consecutive annual outflow of global gold ETFs, led by Europe, with outflows of $11 billion - the worst year since 2013 - and North America (-$10 billion). Asia stood out as the only region to attract inflows (+$1 billion) (source: Bloomberg).

The outflows were driven by the higher opportunity cost of holding gold relative to assets such as US Treasuries, and only partly offset by purchases made at times when gold fully fulfils its function as a haven asset, such as when the dollar is weak, expectations of interest rate cuts intensify, or markets become more turbulent.

Three consecutive years of outflows led global gold ETFs to lose $27 billion over the period, while holdings shrank by $543 trillion. A trend that negatively affected the value of gold (source: Bloomberg).

Considering the three factors described, what are the prospects for gold?

The market consensus today anticipates a 'soft landing' in the United States, which should positively impact the global economy. Traditionally, soft landing scenarios are not particularly favourable for gold, resulting in flat or slightly negative returns. But every cycle is different. The escalation of geopolitical tensions in a key election year for many major economies, combined with ongoing purchases by central banks, could provide further support for gold. Moreover, the likelihood of the Fed guiding the U.S. economy to a safe landing with interest rates above 5% is by no means certain. And a global recession is still a possibility to be monitored. Finally, as mentioned, the potential reversal of trends in financial flows, which penalized gold in 2023, could be a positive factor supporting gold.

At Plenisfer, we believe that, despite the evolution of the macro context, gold has the potential for appreciation due to the persistence of uncertainties on various fronts and the factors described. In any case, we think that gold can consistently remain above the $2,000 per ounce mark and, most importantly, fulfil the important role of stabilizing investors' portfolios.

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and is not a marketing communication relating to a Fund, investment product or investment services in your country. This document does not constitute an offer or invitation to sell or buy any securities or any business or enterprise described herein and does not form the basis of any contract.

Any opinions or forecasts provided are accurate as of the date specified, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance does not predict future returns. There can be no assurance that an investment objective will be achieved or that there will be a return on capital. This analysis is addressed exclusively to professional investors in Italy pursuant to the Markets in Financial Instruments Directive 2014/65/EU (MiFID). It is not intended for retail investors or US Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended.

The information is provided by Plenisfer Investments, authorized as a UCITS management company in Italy, regulated by the Bank of Italy - Via Niccolò Machiavelli 4, Trieste, 34132, Italy - CM: 15404 - LEI: 984500E9CB9BBCE3E272.

All data used in this analysis, unless otherwise indicated, is provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.