Marco Mencini, Head of Research at Plenisfer Investments SGR

2025 is set to be a "golden year": after the first rate cut by the Federal Reserve in mid-September, gold has exceeded the $3,8001 per ounce threshold, reaching USD 3,870 today, a new all-time high in both nominal and real terms.

Gold has already gained around 50% year-to-date, having doubled in price over the past three years1. It is a rally that has few precedents, such as the one recorded after the suspension of the Bretton Woods agreements in the 70s, when the convertibility of the dollar into gold ended.

Will the rally continue?

We remain constructive on gold in light of structurally strong purchases by central banks (which have led 94%1 of the rally since 2022, quintupling their purchases after freezing Russian dollar assets), as well as financial investors.

In particular, year-to-date gold ETFs have attracted $25-30 billion in investment, which equals about 10%1 of a year's mining production, while hedge funds have concentrated nearly half of their entire commodity exposure in US markets on gold1.

In this scenario, the market is already anticipating the next US interest rate cuts, which could be more substantial now that President Trump's trusted adviser, Stephen Miran, is on the Central Bank's board. Not to mention that Jerome Powell's term as Chair is due to expire next May. A less restrictive monetary policy could lead to higher inflation and, therefore, higher long-term rates, resulting in lower bond prices, falling equity markets and an erosion of the dollar's reserve currency status. This should be a favourable environment for safe haven assets: it is estimated that if only 1% of the private capital currently invested in the US Treasury were diverted to gold, the price would rise to almost 5,0002 dollars per ounce.

How to expose yourself to gold?

The market offers two financial alternatives for exposure to gold: producer stocks and ETFs.

Despite the strong year-to-date performance of producer stocks, their valuations remain attractive, with many companies generating free cash flow yields (FCFs) between 7-9%1 (high single digit) and 10-12%1 (low double digit) of their market capitalization. The figure varies between companies, but, also in light of the low leverage, the current levels offer favourable prospects.

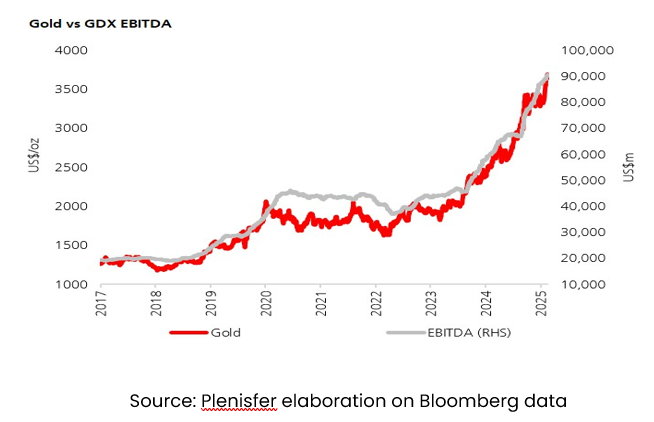

It is believed that the profitability of gold producers cannot keep pace with the price of the metal. However, the EBITDA data of the industry's leading ETFs (GDX, VanEck Gold Miners ETF) belie this perception:

[1] Source: Bloomberg

[2] Source: Goldman Sachs

Today gold’s rise has coincided with a phase in which producers' costs have remained reasonably stable, and therefore their margins have begun to widen significantly3. The new significant generation of cash flows is also leading operators to restart distributing dividends and buyback plans, both of which were largely absent in the last gold rally that took place between the end of 2023 and the beginning of 2024. Those who benefited most from this dynamic were the operators positioned higher up the cost curve, for whom margins reached levels not seen since the 1980s.

At Plenisfer, we believe that this margin expansion is here to stay: structurally, supply is so inelastic that even when prices double, production barely moves, for several reasons:

Extraction is becoming increasingly difficult: in the 1980s, 7-8 grams of gold were present in each ton extracted according to the World Gold Council, which has dropped to about 1-1.5 grams today.

Development times for new mines are long and permitting procedures are increasingly complex: from discovery to production, it often takes up to 15 years.

Capital and risk intensity: Mine development costs billions, and inflation and price volatility can make it difficult to plan such a long-term investment.

Operational rigidity: Productivity is often limited by plant design, safety and reservoir quality.

Geopolitical and regulatory risks: Many mines are in countries with high political and environmental complexity.

Finally, the sector is now characterised by greater concentration and renewed budgetary discipline. At the recent Denver Gold Forum, producers seemed focused on existing projects and opportunities for organic growth, with exploration remaining a key focus. Signs of more sustained M&A activity, rising costs or a correction in the price of gold will be the signals to watch when assessing any exposure to sector players.

[3] Source: Bloomberg

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and is not a marketing communication relating to a Fund, investment product or investment services in your country. This document does not constitute an offer or invitation to sell or buy any securities or any business or enterprise described herein and does not form the basis of any contract.

Any opinions or forecasts provided are accurate as of the date specified, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance does not predict future returns. There can be no assurance that an investment objective will be achieved or that there will be a return on capital. This analysis is addressed exclusively to professional investors in Italy pursuant to the Markets in Financial Instruments Directive 2014/65/EU (MiFID). It is not intended for retail investors or US Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended.

The information is provided by Plenisfer Investments, authorized as a UCITS management company in Italy, regulated by the Bank of Italy - Via Niccolò Machiavelli 4, Trieste, 34132, Italy - CM: 15404 - LEI: 984500E9CB9BBCE3E272.

All data used in this analysis, unless otherwise indicated, is provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.