Carlo Gioja, Senior Portfolio Manager, Plenisfer Investments SGR

The Year of the Fire Horse is shaping up to be a race between two very different breeds.

On one side of the Pacific, US tech companies are investing vast amounts of capital in advanced chips and model development in pursuit of Artificial General Intelligence, or "God-in-a-Box." This is driving up equipment prices and stretching company budgets.

On the other side of the ocean, China is working to make AI inference widely available at the lowest possible cost and to accelerate adoption at scale.

These distinct approaches are driven by both cultural elements and structural differences.

Historically, in China, companies never developed the habit of paying for software. The SaaS (Software as a Service) industry in China has long had a monetisation problem, and to this day, industry revenues are roughly one order of magnitude smaller than those of the US. Consequently, the direct monetisation of Large Language Model (LLM) products through retail and corporate subscriptions is much more challenging in China, forcing model developers to take the open-source path.

More importantly, structural differences in the two economies also drive strategic choices. While the US has the best chips for AI, China has a much bigger installed power capacity. While China struggles to make advanced chips as it's cut off from the leading global semiconductor equipment suppliers, the US faces a major energy supply bottleneck, making the rollout of AI difficult and expensive.

To a degree, the AI race is about whether the US will solve its power woes before China figures out how to make the chips.

In January 2025, China's DeepSeek seemingly came out of nowhere with the release of R1, a model that roughly matched the performance of OpenAI's then-best model, o1, but at a fraction of the cost. The release of R1 showed that open-weight, low-cost models can get very close to the development frontier and can be good enough for most commercial applications. Suddenly, the winner-takes-all dreams of the leading US AI labs looked far less certain.

A year later, China still lacks advanced US chips and Chinese models remain heavily censored, seizing up at the mention of Tiananmen Square, a never-ending source of amusement for Western sceptics. DeepSeek and other Chinese developers have allegedly been caught "cheating" by using leading US models to train their own.

Yet, innovation is born of scarcity.

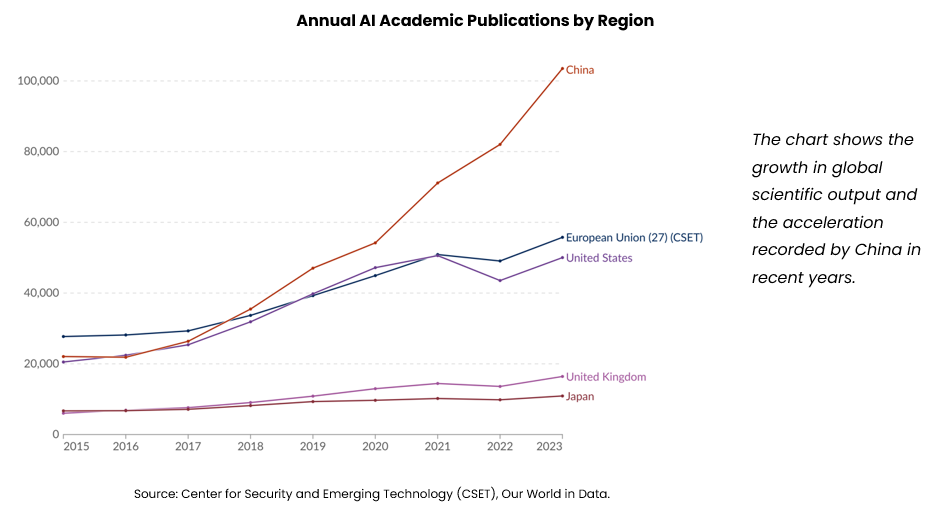

The lesson of the “DeepSeek shock” was not that ambitious startups cut corners, but rather that algorithmic innovation can make up for hardware constraints. And what if the DeepSeek Moment wasn't just a technical breakthrough, but the symptom of an ecosystem reaching critical mass? The growth in scientific output in artificial intelligence underscores the rapid expansion of China’s research and innovation ecosystem in recent years.

China’s 15th Five-Year Plan (2026–2030), expected to be approved by the National People’s Congress in March, zeroes in on "embodied AI" as the country's strategic goal: the rapid integration of AI into as many products and services as possible, as quickly as possible. In line with this aim, AI models are seen as national infrastructure, a basic commodity serving as a foundational layer for the entire economy, much like electricity or steel.

In 2025, the country added roughly half a terawatt of capacity, or about 50% of the entire US grid. Under the "East Data West Computing" initiative, workloads are moving from the developed eastern seaboard (Shanghai, Shenzhen) to energy-rich Western regions via high-speed data and power lines. To address monetisation and adoption challenges, local governments have ramped up subsidies for token use and cloud storage. These subsidies are explicitly intended to "buy time" for the domestic chip industry to catch up with Nvidia's best chips in terms of power efficiency. And the national government is now clearly signalling that domestic companies should buy domestic hardware.

In the meantime, Chinese labs have become exceptionally good fast followers, finding innovative algorithmic solutions that lower compute requirements while achieving comparable performance. Within weeks of Anthropic's release of Opus 4.6, which sparked panic in markets about the "old" software industry, Zhipu AI has introduced a model with performance comparable to leading high-end systems, while aiming to significantly reduce inference costs. Shortly after Google unveiled Genie 3 for world simulation, ByteDance released Seedance 2, which can turn a simple storyboard into a full cinematic preview complete with sound and dialogue. As I write this, DeepSeek is expected to release its V4 model, which will likely further reduce inference costs.

The promise of open-source and rapid adoption at scale ("embodied AI") is that greater adoption leads to better hardware economics, better data, more edge cases, and more algorithmic innovation, which, in turn, leads to better models in a virtuous loop.

Hence, scaling adoption quickly is not just about using up existing capacity but is also a way to accelerate model development. If the new generation of agents can learn to manage a manufacturing line, for example, operate autonomous robots or run a pharmaceutical trial, the increase in productivity could well pay for the initial effort, making Chinese products and services much more competitive globally.

A generation ago, the world economy became addicted to cheap Chinese manufacturing. What if it becomes hooked on Chinese compute?

It may be tempting to assume current geopolitics will make the Chinese approach untenable, limiting the potential for overseas expansion of these technologies. While the property crisis is still acting as a massive drag on economic growth, the challenges facing the country's AI strategy are real, the decision-making process is far from perfect, and the lack of transparency on the levels of state support around training and inference makes any straightforward economic calculation very difficult.

Yet, as investors, we also note that even a partial success scenario is far from being priced in. As per Bloomberg data, MSCI China currently trades at 12x 2026 earnings versus the SP500 at 22x, for roughly comparable mid-double-digt expected growth. If Beijing's AI gambit works, Chinese productivity could reaccelerate meaningfully over the next decade.

The beneficiaries will not necessarily be the providers of the AI infrastructure or the model makers either. The government's goal is to make benefits accrue to the economy at large and trickle down to many more sectors, such as manufacturing and healthcare. In the 2000s, the state subsidised the production of critical resources such as steel enabling local champions to dominate industries such as shipbuilding, logistics and modern manufacturing. Now, the true value of Chinese AI may also be captured downstream, by companies that apply cheap inputs to strengthen their competitive advantages further.

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and does not constitute a marketing communication relating to a fund, an investment product or investment services in your country. This document does not constitute an offer or invitation to sell or purchase securities or any assets or businesses described herein and does not form the basis of any contract. Any opinions or forecasts provided are as of the specified date, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance is not indicative of future returns. There can be no guarantee that any investment objective will be achieved or that capital will be returned. This analysis is intended exclusively for professional investors in Italy pursuant to Directive 2014/65/EU on markets in financial instruments (MiFID). It is not intended for retail investors or U.S. Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended. Information is provided by Plenisfer Investments, authorised as a UCITS management company in Italy and regulated by the Bank of Italy – Via Niccolò Machiavelli 4, Trieste, 34132, Italy – CM: 15404 – LEI: 984500E9CB9BBCE3E272. All data used in this analysis, unless otherwise stated, are provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.