Mauro Ratto, Co-CIO Plenisfer Investments SGR

After last year’s peaks, inflation is set to moderate, but we do not believe it will return to previous levels. We think inflation will remain a structural component of the Western economy.

Central Banks will face a complex challenge. They cannot be too restrictive without penalizing the economy, which we expect to slow down, especially in the US. Moreover, they cannot implement overly expansive policies without accelerating inflation. There will be moderate rate cuts, but rates will remain higher for longer, particularly in the US, where inflation is a direct consequence of demand supported by public incentives.

Markets have already priced in this scenario, as evidenced by the relative strength of the dollar compared to the euro. This is reflected in the yield differential between Europe and the United States, and between the United States and Emerging Markets, which are now at historical lows.

In this scenario, we look at the short and medium-term part of the curve, which, combined with credit risk, offers attractive yields in Europe and in the US. In fact, we have built a steepening position. Given the context of significant and constantly growing public deficits, we expect that to make long-term maturities attractive, a maturity premium will need to be restored.

In emerging markets, there are selected opportunities in dollar-denominated issues with an attractive risk-reward profile and offer a unique combination of country spreads and US base rates. However, credit spreads are at their lowest since 2018, so great caution is needed.

In bond markets, we believe that interesting opportunities characterized by contained volatility can be mainly found by moving down the capital structure of bond issuers.

To seize these opportunities, however, a benchmark-free approach and a comprehensive analysis of the issuing company are required, extending beyond the sole issuance to include the creditworthiness and overall characteristics of the company.

With this approach, we specifically look at so-called “hybrid bonds” i.e., junior bonds in the capital structure, typically long-term or perpetual, linked to explicit short-term call options by the issuer. These calls are usually respected as non-calling (so-called “reset”) would be costly for the issuer.

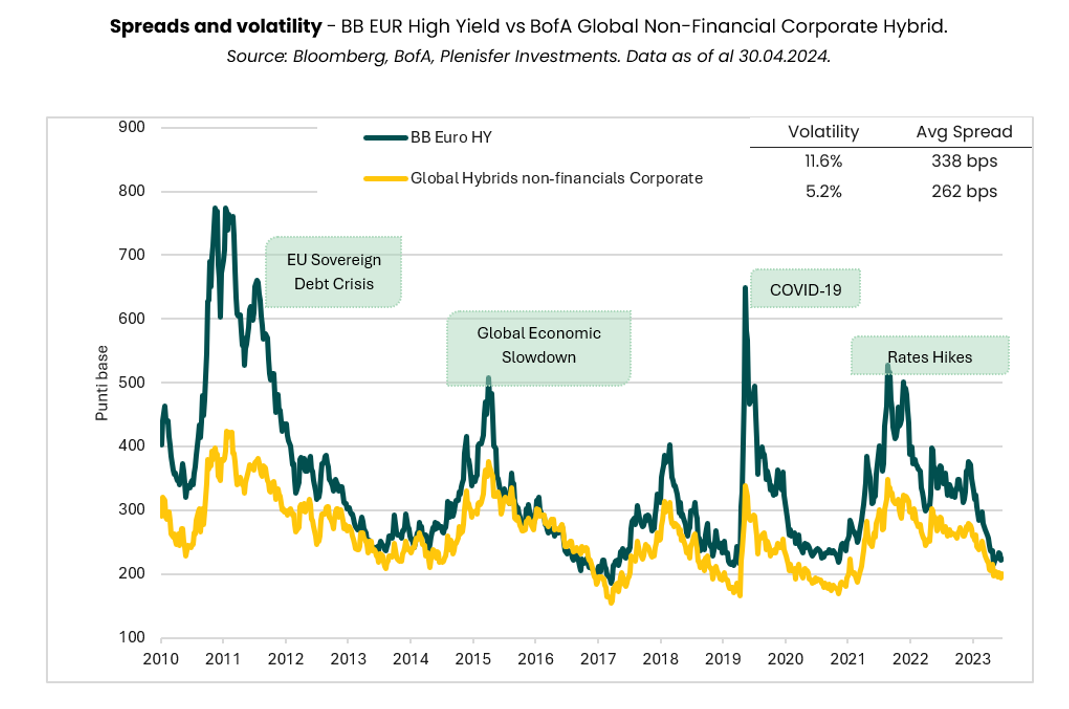

Analysing the spread dynamics of the global non-financial hybrid bonds index relative to the European BB high yield index (so-called “crossover”) – which offers similar yields in terms of spread – it emerges that the volatility profile of hybrid bonds is more than 50% lower:

Reasons for this dynamic include four distinctive factors that characterize non-financial hybrids compared to high yield bonds:

1. Better Credit Quality of Issuers

Non-financial hybrid issuers tend to have higher credit ratings than high yield issuers.

2. Stronger Balance Sheets and Better Long-Term Prospects

Non-financial hybrid issuers are typically mature companies with significant cash flows, operating in established sectors. In contrast, high yield issuers are generally concentrated in higher-risk sectors and are more vulnerable to economic downturns.

3. Lower Sensitivity to Interest Rate Dynamics

During phases of accommodative monetary policy, demand for hybrid bonds remains stable as investors seek alternatives with higher yields than government bonds, helping to reduce volatility. In turbulent times, non-financial hybrids offer a perceived adequate yield relative to risk, favouring price stability compared to high yield bonds, which may be more prone to heavy selling.

4. Shorter Duration of Hybrids

Due to call options, hybrids have less exposure to interest rate risk.

Considering the uncertainty over future monetary policy dynamics, we continue to maintain a conservative stance regarding market expectations on the extent and timing of rate cuts. We prefer exposure with shorter duration.

In this context, navigating the global bond market, we believe that with an active, benchmark-free approach, opportunities can be seized related to the yield level offered by non-financial hybrids and their limited exposure to interest rate risk.

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and is not a marketing communication relating to a Fund, investment product or investment services in your country. This document does not constitute an offer or invitation to sell or buy any securities or any business or enterprise described herein and does not form the basis of any contract.

Any opinions or forecasts provided are accurate as of the date specified, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance does not predict future returns. There can be no assurance that an investment objective will be achieved or that there will be a return on capital. This analysis is addressed exclusively to professional investors in Italy pursuant to the Markets in Financial Instruments Directive 2014/65/EU (MiFID). It is not intended for retail investors or US Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended.

The information is provided by Plenisfer Investments, authorized as a UCITS management company in Italy, regulated by the Bank of Italy - Via Niccolò Machiavelli 4, Trieste, 34132, Italy - CM: 15404 - LEI: 984500E9CB9BBCE3E272.

All data used in this analysis, unless otherwise indicated, is provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.