Marco Mencini, Head of Research, Plenisfer Investments SGR

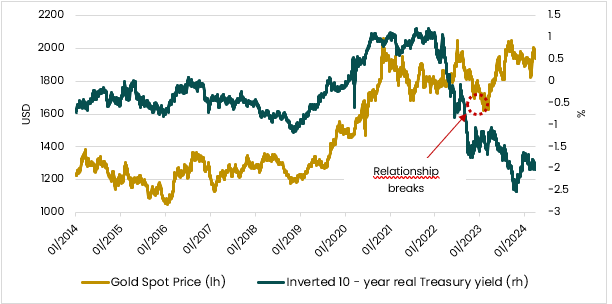

In a recent commentary we examined the factors influencing the price of gold: the most relevant is the gold purchase made by central banks, which since 2022 exceeds 1,000 tons annually, an amount representing about 30% of annual production. And it is precisely this factor that has led to the breaking of the historical correlation between interest rates and gold*:[1]

[1] *Source: Bloomberg

Source: Bloomberg and Plenisfer Investments. Data as of 3rd April 2024

If the historical correlation were still in effect, the current level of interest rates would lead to a decrease of 500-600 dollars per ounce in the price of gold*, while since 2022 gold has followed an upward trajectory, reaching $2,300 today.

A record, however, only apparent when compared to past values normalized for inflation: during the sovereign debt crisis, between 2011 and 2014, gold reached $2,500 per ounce*.

Given this positive trend, the disappointing stock performance of gold producers may therefore seem anomalous: while gold has grown by 31% in the last three years, during the same period the sector remains flat, despite a historical beta of 1.5 times the price of gold*

But for mining companies, there could be a light at the end of the tunnel.

In the past, the rapid appreciation of gold led operators to carry out costly mergers and acquisitions and to make aggressive operational decisions; however, in the current cycle, balance sheet discipline has remained strong, with a focus on prioritizing free cash flow over revenues. Capital expenditure and debt levels are also now well below the levels reached in the last cycle (2016-2021), and the majority of producers have a net debt to EBITDA ratio of less than 0.5*. Today most historical producers aim to sustain production rather than pursue growth at any cost.

So, what is behind the disappointing stock performance of operators? It is due to margin contraction, connected to the increase in production costs.

The question we ask ourselves today when looking at the sector is therefore how likely it is for margins to improve.

On one hand, the probabilities are obviously linked to the general trend of inflation, but we believe that costs on the energy and equipment fronts may have already peaked, and therefore the peak of cost inflation may be behind us. Based on indications provided by companies, we also estimate that cost inflation may decrease gradually in 2025, largely due to expected increases in production.

Operators, however, have another card up their sleeve, namely the possibility of closing or divesting high-cost extraction activities. This possibility is especially valuable for operators with a diversified portfolio of mining deposits who may move in this direction to improve their profitability.

Below-Average Historical Valuations

Today, the leading gold producers are trading at 5.5 times the Enterprise Value to EBITDA ratio for 2025, well below the historical average of 7-8 times*. We have to go back a decade to find the last four instances where the gap between the value of gold and the stock prices of companies in the sector became so wide*. On those occasions, we witnessed a subsequent average increase of 25% in the price of gold and over 60% in the main ETF dedicated to the sector*.

In conclusion, at Plenisfer, we believe that, in light of the factors described, there is potential for appreciation of the producing companies towards a more correct alignment with the price of gold.

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and is not a marketing communication relating to a Fund, investment product or investment services in your country. This document does not constitute an offer or invitation to sell or buy any securities or any business or enterprise described herein and does not form the basis of any contract.

Any opinions or forecasts provided are accurate as of the date specified, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance does not predict future returns. There can be no assurance that an investment objective will be achieved or that there will be a return on capital. This analysis is addressed exclusively to professional investors in Italy pursuant to the Markets in Financial Instruments Directive 2014/65/EU (MiFID). It is not intended for retail investors or US Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended.

The information is provided by Plenisfer Investments, authorized as a UCITS management company in Italy, regulated by the Bank of Italy - Via Niccolò Machiavelli 4, Trieste, 34132, Italy - CM: 15404 - LEI: 984500E9CB9BBCE3E272.

All data used in this analysis, unless otherwise indicated, is provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.