Marco Mencini, Head of Research at Plenisfer Investments SGR

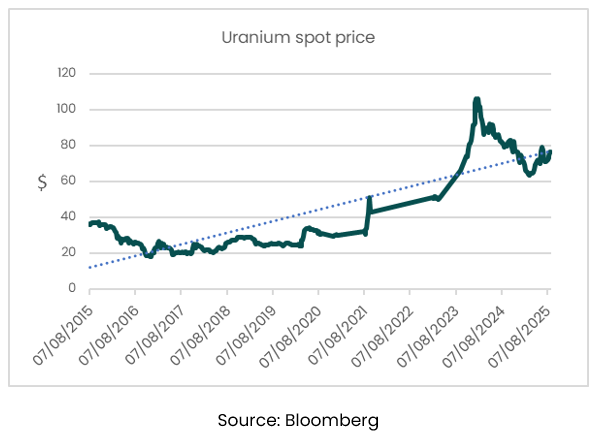

Over the past twelve months, there has been the gradual consolidation of uranium spot prices to around $70 per pound, more than double the average price of around $30 recorded between 2016 and 2021, but still far from the peak in early 2024 of over $100[1]:

[1] Source: Bloomberg

Does this mean that the current price is the new reference value for uranium, and that the 2024 peak was an isolated case?

In our view, no.

The recent fall in prices is due to short-term dynamics. The 2024 peak was supported by massive purchases by utilities, but over the past 12 months, these utilities have been limiting their procurement activity. This procurement activity has been below the replacement rate of stocks[2], as they have been waiting for prices to fall.

A drop, in our view, unlikely.

In fact, we believe that the current market phase is a physiological pause following an acceleration of more than two years, and it does not alter the trajectory of the current secular cycle.

At Plenisfer, we consider $70 to be the new minimum price for uranium and expect it to gradually rise towards $80 in the short term and towards $100 in the medium term. This estimate is supported by analysis of industry dynamics and fundamentals.

The factors supporting a growing demand

The uranium deficit remains structural: global demand is growing steadily and is estimated at around 195 million pounds in 2025, compared to primary production of between 155 and 160 million. The annual deficit therefore exceeds 30 million pounds[1].

Indeed, demand continues to be driven by new energy policies: 63 plants are under construction worldwide, while Japan has reactivated 25% of its existing plants - shut down after the Fukushima disaster - and has confirmed that it will reach 100% within the decade, before starting to build new plants[3]. China aims to build 150 plants by 2040, tripling its demand for uranium[4], and in Europe we are witnessing the growing interest in nuclear power and in the latest generation of production systems, the Small Modular Reactor (SMR).

And supporting demand is now a new key player: the United States.

The 'Trump Act' and the American nuclear renaissance

Through the Executive Orders of 23 May 2025, Trump unveiled a strategic plan aimed at quadrupling US nuclear capacity from 100 to 400 GW by 2050[5]. He introduced a fast-track licensing process for new plant construction, a pilot programme for three modular reactors to be built within a year, upgrades to existing plants, and initiatives to reopen closed plants. He also introduced programmes to support the domestic uranium industry.

This is a historic turning point. Not only is the US returning to massive investment in nuclear power, it is also doing so with a strategic vision of energy independence and technological leadership. Together with China, the two Countries alone have set a cumulative target of over 1,200 GW of nuclear capacity by 2050, up from around 390 GW today[6]. This implies a potential demand for over 1 billion pounds of uranium over the next 15 years.

In addition to this, major technology companies will generate further demand: Microsoft, Google and Amazon plan to invest over USD 1 trillion in new data centres over the next five years to support the development of artificial intelligence systems. To power these systems, they have already invested or announced investments in existing power stations or SMRs totalling over USD 3 billion[3].

What about supply?

Primary production is largely insufficient today, but supply is slow to react. To open new mines, not only does it take a long time (10-15 years) but it also requires uranium prices that make the investment economically viable.

Kazatomprom, the world's largest producer with more than 40% of the market, recently confirmed a 10% reduction in production in 2026, given the need of permanently higher prices of at least $80 to return to 100% underground utilisation.

In addition, the secondary market, which has so far compensated for the shortage of supply, is set to dry up: Japan - one of the main suppliers of unused uranium stocks following the shutdown of the country's power plants - is now reactivating its own plants.

On top of this, large financial players continue to hoard physical uranium off the market, further reducing its availability.

Conclusion: a reinforced view

In the short term, price volatility can offer attractive entry points. But it is in the medium to long term that uranium shows its true potential. Current levels, which are below the peaks of 2024 and still a long way from the real historical highs ($137 per pound in 2007[5], equivalent to over $180 today when adjusted for inflation), represent an interesting opportunity, also in light of the issues it can combine:

- clear and measurable long-term trends (decarbonisation, energy security, AI infrastructure, defence);

- a limited, rigid and slow-reacting supply;

- a still present undervaluation compared to the equilibrium fair value.

Any additional sanctions imposed on Russia could also accelerate the price run-up towards the $100 per pound target, which is equal to the operating cost of production for smaller players.

We remain, therefore, constructive on uranium, the price of which we estimate will gradually rise again over the next 12 months as utilities, characterised by medium-term buying cycles, return to buy uranium after a year of substantial immobility and face an increasingly thin market.

The window of opportunity to seize the uranium outlook is now: the secular uranium cycle is not over, it is just catching its breath.

[1] Source: Bloomberg

[2] Source: Sprott

[3] Source: International Energy Agency

[4] Source: China Atomic Energy Authority

[5] Source: Bloomberg

[6] Source: International Energy Agency

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and is not a marketing communication relating to a Fund, investment product or investment services in your country. This document does not constitute an offer or invitation to sell or buy any securities or any business or enterprise described herein and does not form the basis of any contract.

Any opinions or forecasts provided are accurate as of the date specified, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance does not predict future returns. There can be no assurance that an investment objective will be achieved or that there will be a return on capital. This analysis is addressed exclusively to professional investors in Italy pursuant to the Markets in Financial Instruments Directive 2014/65/EU (MiFID). It is not intended for retail investors or US Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended.

The information is provided by Plenisfer Investments, authorized as a UCITS management company in Italy, regulated by the Bank of Italy - Via Niccolò Machiavelli 4, Trieste, 34132, Italy - CM: 15404 - LEI: 984500E9CB9BBCE3E272.

All data used in this analysis, unless otherwise indicated, is provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.