Mauro Ratto, Co-Founder and CIO, Plenisfer Investments SGR

For decades, the US dollar has represented an exception in modern financial history, as the only currency able to strengthen and maintain a central role despite imbalances that, in any other country, would have undermined its credibility: rising public debt and a chronic, widening budget deficit, accompanied by a persistent current account deficit.

The reason behind this anomaly, often described as the “dollar privilege”, goes beyond the economic strength of the United States and lies primarily in the ability of the US system to attract global capital. The Treasury market continues to represent the concept of a risk‑free asset, while US equities have for years been the main driver of returns, liquidity and innovation, to the point of accounting for more than 60% of global market capitalisation[1]. Together, these two factors have generated financial inflows sufficient to offset imbalances that would be unsustainable elsewhere.

Since the United States requires foreign capital to finance its fiscal and trade deficits, the strength of the dollar depends on the continuity of these flows. When they slow or come to a halt, structural fragilities inevitably emerge.

This occurred in 2000, in 2008 and, more recently, in April 2025, when the announcement of new trade tariffs by the US administration triggered a period of market tension and a temporary reduction in international exposure to US assets.

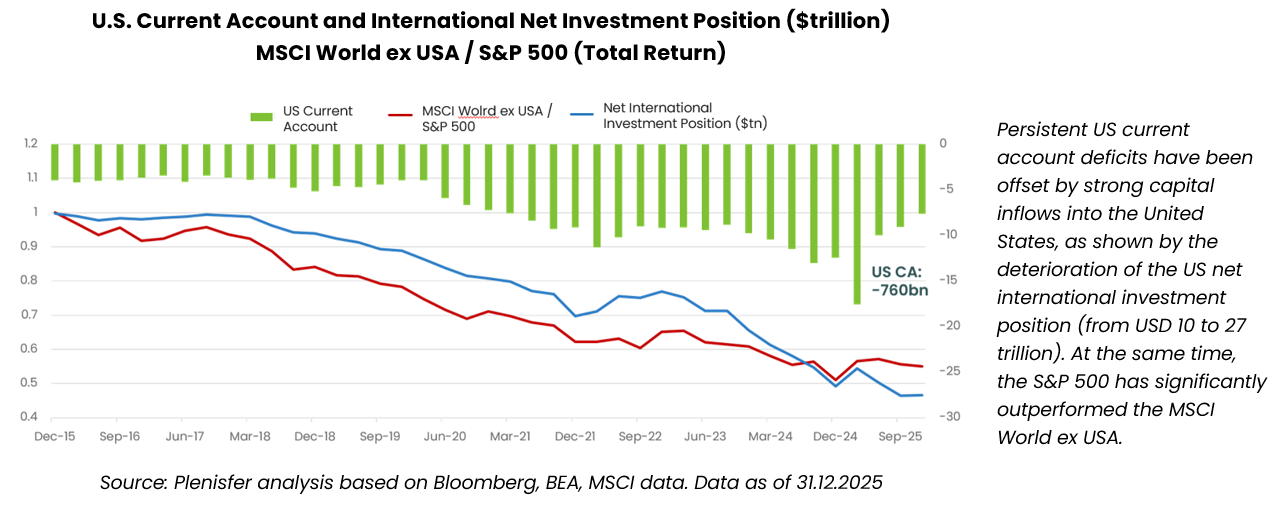

This situation is reflected in the US net international investment position, which has reached USD 27 trillion, rising sharply since 2020 (USD 20 trillion)[2]. In a “normal” economy, such a large and deteriorating negative net position vis‑à‑vis the rest of the world would be a precursor to a currency crisis. In the case of the United States, however, the role of the dollar as the world’s main reserve currency continues to sustain international demand for US assets, thus preventing this outcome so far. Nevertheless, the rapid expansion of the negative position and the growing equity component of liabilities – also fuelled by the surge in technology and artificial‑intelligence‑related stocks – make the United States more exposed to equity market corrections and accentuate its long‑term vulnerabilities.

US equity markets remain characterised by high valuations and increasing concentration. US economic growth also appears more concentrated than the aggregate data suggest: in the first quarter of 2026, real GDP grew at an annualised rate of 2.0%, with investment contributing 1.48 percentage points[3] — the most significant component of growth. Within this category, AI‑related investment is by far the dominant driver. This model remains sound as long as global capital continues to flow into the United States.

Geopolitics has changed the perception of the dollar

The freezing of Russian dollar‑denominated reserves following the invasion of Ukraine marked a turning point for many central banks and emerging countries. From that moment, a slow but steady process of diversification of global foreign‑exchange reserves began. The most visible consequence has been increased purchases of the only real asset without counterparty risk, namely gold, by emerging‑market central banks. Over the past ten years, China has significantly reduced its direct exposure to US Treasuries, from a peak of over USD 1.3 trillion to just under USD 700 billion today[4], the lowest level since 2008 – while total foreign‑exchange reserves have remained broadly stable at around USD 3.3–3.4 trillion, still largely denominated in dollars[5].

In recent months, the dollar has shown that it still retains the ability to strengthen during periods of global systemic crisis. Tensions related to the conflict in Iran and risks surrounding the Strait of Hormuz temporarily brought the greenback back to the centre of defensive international flows, supporting the Dollar Index (DXY) after months of weakness[6]. However, unlike what occurred during Covid or the 2022–2023 tightening cycle, recent shocks have resulted in only a moderate and volatile strengthening of the dollar, and a much less pronounced weakening of emerging‑market currencies.

The difference compared with the past does not lie in the dollar’s function: its strength in crisis phases is now less evident, signalling a safe‑haven role that is still present but less “mechanical” and more selective.

The most important change comes from emerging markets

In the past, the dollar was the backbone of emerging‑market economic development: countries with high growth potential but limited domestic savings were forced to borrow abroad by issuing dollar‑denominated debt. This created a strong currency mismatch, as debt was in dollars while most revenues and investment flows were generated in local currency. In practice, many emerging economies were structurally “short” dollars. During periods of stress, the need to close these positions and obtain dollars to refinance or repay debt fuelled the classic fly to quality: forced sales of local assets, capital flight and further appreciation of the greenback.

Today the landscape is profoundly different. Many emerging countries have developed a more solid domestic savings base, more mature financial markets and local investors capable of absorbing bond issuance in local currency. The result is a progressive reduction in dollar‑denominated debt.

In 2025, net issuance of external hard‑currency debt by emerging markets turned negative – a structurally significant signal – while issuance in local currency increased [7]. According to the IMF, the share of debt issued in USD has fallen to multi‑year lows in many countries, confirming this trend. Emerging markets are increasingly less dependent on dollar financing than in the past and, consequently, less exposed to the structural need to purchase US currency.

The euro and emerging‑market currencies regain relevance

In this context, the relative behaviour of other currencies is also changing. The euro, for example, has shown surprising resilience even in the presence of significant geopolitical shocks. Similarly, some emerging‑market currencies, such as the Brazilian real and the Mexican peso, have displayed much greater resilience than in previous cycles.

This is an important signal, showing that dollar appreciation is no longer the only possible response in times of uncertainty. The search for diversification increasingly supports other currency areas as well.

Moreover, the gradual realignment of European interest rates with US rates reduces one of the dollar’s main competitive advantages of recent years.

The dollar will not lose its status as a store of value, but its weakening will reflect a more multipolar world from a currency perspective as well.

The impact of the new currency regime on portfolios

In a world characterised by high debt, more persistent inflation, geopolitical tensions and less synchronised growth, currency diversification once again becomes a strategic rather than merely tactical component.

For investors, this means paying closer attention to emerging‑market local‑currency bonds, certain cyclical currencies linked to commodities, gold and real assets capable of preserving value in the current environment.

The construction of global portfolios could also change profoundly. While in recent years concentration in the United States was almost automatically rewarded, the next cycle may require greater geographic, sectoral and currency diversification.

The dollar will likely remain at the centre of the global financial system for a long time. But for the first time in decades, the market is questioning the sustainability of its exceptional status.

[1] Source: Plenisfer Investments based on MSCI ACWI Index data, free-float market capitalization

[2] Source: U.S. Bureau of Economic Analysis (BEA), U.S. Net International Investment Position

[3] Source: U.S. Bureau of Economic Analysis (BEA), Gross Domestic Product, First Quarter 2026 (Advance Estimate)

[4] Source: U.S. Department of the Treasury, Major Foreign Holders of Treasury Securities (TIC data)

[5] Source: State Administration of Foreign Exchange (SAFE), China Foreign Exchange Reserves

[6] Source: Bloomberg, U.S. Dollar Index (DXY)

[7] Source: UBS Research, Barclays Research, International Monetary Fund (IMF)

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and does not constitute a marketing communication relating to a fund, an investment product or investment services in your country. This document does not constitute an offer or invitation to sell or purchase securities or any assets or businesses described herein and does not form the basis of any contract. Any opinions or forecasts provided are as of the specified date, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance is not indicative of future returns. There can be no guarantee that any investment objective will be achieved or that capital will be returned. This analysis is intended exclusively for professional investors in Italy pursuant to Directive 2014/65/EU on markets in financial instruments (MiFID). It is not intended for retail investors or U.S. Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended. Information is provided by Plenisfer Investments, authorised as a UCITS management company in Italy and regulated by the Bank of Italy – Via Niccolò Machiavelli 4, Trieste, 34132, Italy – CM: 15404 – LEI: 984500E9CB9BBCE3E272. All data used in this analysis, unless otherwise stated, are provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

VAT n. & Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.