Marco Mencini, Head of Research, Plenisfer Investments SGR

If 2023 will be remembered as the year of the artificial intelligence breakthrough, the following two-year period has marked its transition from technological promise to a structural pillar of the digital economy. The large-scale adoption of generative models, the expansion of cloud and edge computing, and the growing diffusion of data-intensive applications have made it increasingly clear that the full deployment of AI’s potential is inextricably linked to the availability of reliable, pervasive, low-latency network infrastructures.

Connectivity demand is no longer growing solely in terms of volume, but increasingly in terms of service quality: low latency, operational continuity and the ability to manage ever more complex data flows have become essential requirements for advanced industrial applications, ranging from automated manufacturing to digital healthcare and intelligent mobility. In this context, telecommunications networks represent one of the most strategically important infrastructures for the economic competitiveness of national systems.

However, two years on, the structural weaknesses of the European telecommunications sector not only persist, but in some cases appear more pronounced. Europe continues to suffer from excessive market fragmentation, a legacy of a competitive model that over the past two decades has prioritised price compression at the expense of operators’ profitability.

The paradox is evident: while data traffic continues to grow at a sustained pace and demand for digital services intensifies, telecommunications operators struggle to translate this growth into adequate cash generation. This is compounded by a financial environment that is less accommodative than in the past, where the cost of capital and debt refinancing have become increasingly binding constraints.

In this scenario, some elements of discontinuity are emerging.

First, the debate around sector consolidation has taken a significant step forward. In several European markets, there is growing openness—also at the regulatory level—towards merger transactions that reduce the number of operators, reflecting a broader recognition that a more rational industrial structure is a necessary condition to sustain the investments required by the digital transition. Increasingly, consolidation is viewed not merely as a cost-efficiency tool, but as a process of “market repair”, essential to restoring profitability levels consistent with the highly capital-intensive nature of the sector.

At the same time, the trend towards the separation of network infrastructure and services has strengthened. The entry of specialised investors and long-term capital has supported the development of models in which networks are valued as standalone infrastructure assets, capable of generating stable returns over extended time horizons.

The international comparison further underscores what is at stake. In the United States, a market characterised by a smaller number of operators, the telecommunications sector has benefited from greater investment capacity and better monetisation of the growing demand for advanced digital services. In China, meanwhile, strong state involvement and a concentrated industrial structure have enabled large-scale infrastructure investments, albeit in a context of lower average pricing.

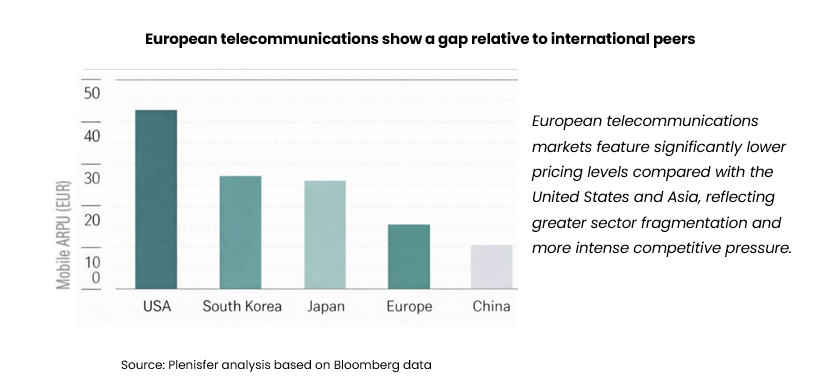

In Europe, by contrast, average telecommunications service prices are structurally lower than in the United States and, in many cases, also lower than in other developed Asian markets, reflecting the sector’s high degree of fragmentation and particularly intense competitive pressure. This dynamic has historically weighed on operators’ profitability and their ability to sustain long-term infrastructure investments.

Against this backdrop, Europe risks falling behind precisely at a time when artificial intelligence is emerging as a key driver of economic growth and geopolitical competitiveness.

This gap reflects a broader challenge affecting the continent’s strategic infrastructure as a whole: the digital and energy transitions are progressing in parallel, yet both risk being slowed by the presence of outdated, fragmented and under-invested physical networks.

In this scenario, the European telecommunications sector stands at a turning point. The approval of the Digital Networks Act (DNA) fits squarely into this transition, representing the first comprehensive attempt at the European level to address the structural industrial challenges of the telecommunications sector and to formally recognise digital networks as strategic infrastructure for economic competitiveness, security, and the development of artificial intelligence.

The development of digital infrastructure fit for the age of artificial intelligence can no longer be postponed and requires a change of pace at both the industrial and regulatory levels.

After a prolonged phase of particularly intensive investment, in several European markets the network build-out cycle is gradually entering a more mature stage. The rollout of next-generation infrastructure (fibre and 5G) allows for a gradual normalisation of capex levels, improving cash-flow visibility and the sector’s financial sustainability.

In this context, consolidation plays a complementary and crucial role: by reducing competitive fragmentation, it can help restore economic conditions more consistent with the capital-intensive nature of the sector, strengthening operators’ ability to remunerate invested capital and to support new investment cycles over the medium to long term—provided an appropriately balanced regulatory framework is in place.

Telecommunications and Energy: a Shared Challenge

According to the European Commission, around 40% of the EU’s electricity distribution networks are now more than 40 years old, highlighting a significant need for infrastructure modernisation (Source: European Commission, European Electricity Grids, 2023). To make electricity grids fit for the growing electrification of consumption and the integration of renewable energy sources, more than €580 billion of investment in transmission and distribution infrastructure will be required by 2030 (Source: European Commission, European Grids Action Plan), with total needs potentially exceeding €1 trillion over a longer-term horizon (Source: ACER – Agency for the Cooperation of Energy Regulators; EIB – European Investment Bank).

Telecommunications and energy therefore share a common challenge: adapting critical infrastructure to structurally growing demand in a context of rapid technological change. Without modern electricity grids, the energy transition cannot be achieved; without resilient, high-performance digital networks, the AI-driven economy risks encountering similar bottlenecks.

In this context, artificial intelligence introduces a new variable into the sector’s risk-return profile. While it does not yet represent a direct revenue driver for most operators in the short term, AI acts as a catalyst for demand for advanced network infrastructure, reinforcing the strategic centrality of these assets and making the unsustainability of purely price-based competitive models increasingly evident. If adequately supported by regulatory evolution, this transformation could translate into greater competitive discipline and, over time, a structural improvement in returns on invested capital.

Implications for Investors

For investment portfolios, the European telecommunications sector should therefore not be viewed as a homogeneous whole. Value creation is likely to be concentrated in specific segments: on the one hand, high-quality infrastructure assets—such as fibre networks, towers, backbone networks and wholesale platforms—that offer cash-flow visibility and more stable return profiles; on the other, integrated operators able to benefit from economies of scale, reduced competitive pressure and a greater ability to monetise value-added services for the corporate segment.

These characteristics largely overlap with those of modern electricity infrastructure, reinforcing the case for thematic exposure to networks as a cornerstone of long-term portfolio construction.

From an asset-allocation perspective, telecommunications and energy can be seen as components of a broader infrastructure allocation, characterised by long investment horizons, high barriers to entry and relatively stable, often regulated or contracted, cash flows. The convergence of the digital and energy transitions strengthens the role of infrastructure as a strategic asset class, potentially offering diversification relative to traditional asset classes and greater protection in scenarios of heightened macroeconomic volatility.

At the same time, however, risks remain significant. High capital intensity, the need for continuous technological investment and uncertainty around the timing and modalities of consolidation require a prudent and selective approach. In the absence of a clear regulatory shift, there is a risk that rising traffic demand continues to translate more into cost growth than margin expansion, delivering limited benefits to shareholders.

From a long-term perspective, we therefore believe that the European telecommunications sector is gradually regaining relevance within diversified portfolios. No longer merely as a defensive segment or a source of dividend income, but as a strategic exposure to infrastructure that is essential to the artificial-intelligence economy. Viewed alongside the ongoing transformation of electricity networks, this evolution points to an increasingly pronounced convergence between digital and energy infrastructure—both of which are necessary to support long-term growth, transition and competitiveness. The combination of compressed valuations, potential industrial catalysts and the growing systemic importance of networks could, over time, create the conditions for a selective re-rating of the sector, benefiting investors with a patient and disciplined time horizon.

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and does not constitute a marketing communication relating to a fund, an investment product or investment services in your country. This document does not constitute an offer or invitation to sell or purchase securities or any assets or businesses described herein and does not form the basis of any contract. Any opinions or forecasts provided are as of the specified date, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance is not indicative of future returns. There can be no guarantee that any investment objective will be achieved or that capital will be returned. This analysis is intended exclusively for professional investors in Italy pursuant to Directive 2014/65/EU on markets in financial instruments (MiFID). It is not intended for retail investors or U.S. Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended. Information is provided by Plenisfer Investments, authorised as a UCITS management company in Italy and regulated by the Bank of Italy – Via Niccolò Machiavelli 4, Trieste, 34132, Italy – CM: 15404 – LEI: 984500E9CB9BBCE3E272. All data used in this analysis, unless otherwise stated, are provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

VAT n. & Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.