Marco Mencini, Senior Portfolio Manager Equity di Plenisfer Investments SGR

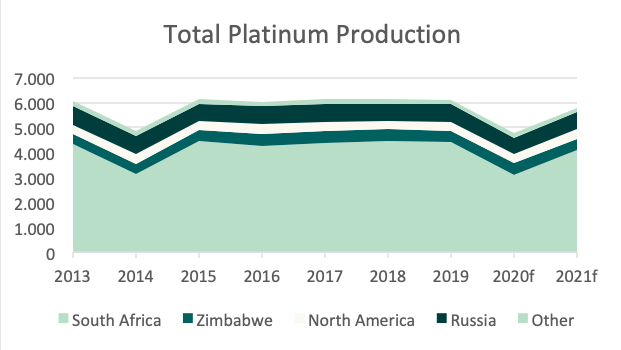

Platinum is rare (only the 72nd most common chemical element in the earth’s crust, out of 92 natural elements) with 80% of the world’s economically viable reserves located in South Africa.

Platinum is prized for its catalytic properties; i.e. its ability to speed up a chemical reaction without itself being changed in the process. Platinum’s physical and catalytic properties mean it has a wide range of uses in industrial and consumer applications, and for investment. Currently, automotive represents the highest end use for platinum (37-41%); followed by jewellery (31-38%).

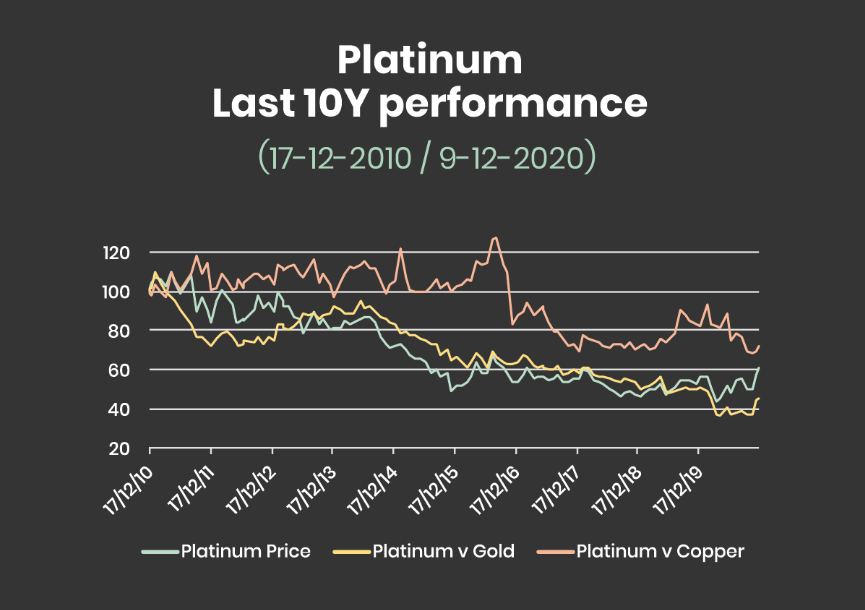

We note persistent concerns over the impact an electrification of vehicles will have on platinum and palladium demand given sales of cars with a combustion engine (i.e. both ICEs and HEVs) may have peaked resulting in dramatic underperformance of Platinum vs both Gold and Copper over the last 10 years.

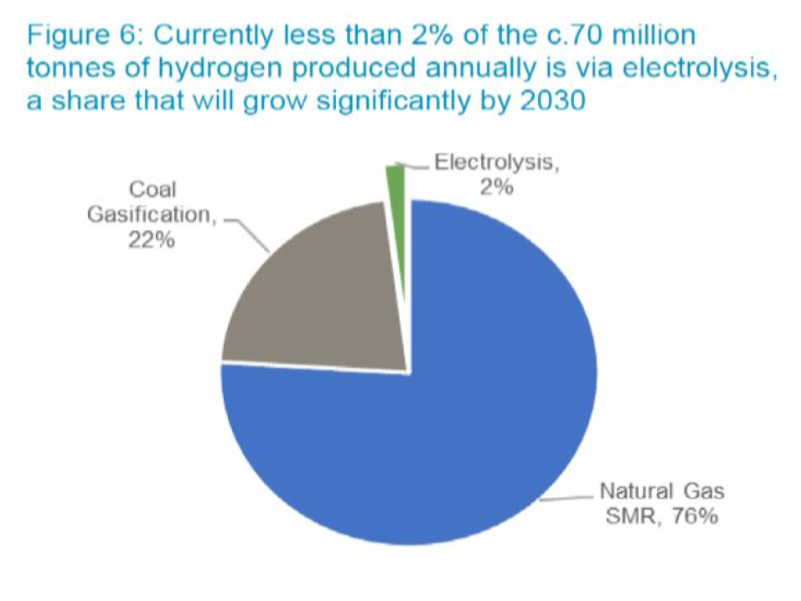

Source: US Dept. of energy, WPIC Research. Note: SMR is Steam Methane Reforming

Source: Bloomberg & Plenisfer Investments SGR 9/12/2020

We believe this doesn’t reflect the complexity of the process. Outside of vehicle numbers and size and powertrain trends, the technological change driven by emissions legislation is a key driver of demand in the auto industry. All else being equal, to achieve lower emissions from a vehicle a higher volume of Platinum content is needed.

Most overlooked by the market appears to be the potential impact of the hydrogen economy. Platinum is crucial for the electrolysis of water using renewable energy to produce ‘green’ hydrogen and technological changes are likely to increase this demand as it replaces iridium. A transition to green hydrogen could achieve material decarbonisation. Based on the current EU and China green hydrogen capacity targets alone would require, cumulatively over 1m oz of platinum by 2030 – about 18% of current mining supply.

Platinum is viewed as an undervalued gold proxy. As the Gold price has moved higher, investors have buying platinum to participate in the move in precious metals.

Over the longer term, the establishment of base demand from the hydrogen economy, coupled with a resurgence in jewellery demand, could lead to material appreciation of Platinum price. This forecast also considers existing supply constraints (80% of supply from South Africa) and long lead time to build new production (i.e. 8 -10years as per one company’s forecast).

Source: WPIC 2019

Disclaimer

This analysis has been prepared for informational purposes only. This document does not constitute an offer or invitation to sell or buy any securities or any business or business described herein and does not form the basis of any contract. The above information should not be used for any purpose. Plenisfer Investments SGR S.p.A. has not independently verified any of the information and does not release.

No representations or warranties, express or implied, as to the accuracy or completeness of the information contained herein and the same (including their respective directors, partners, employees or consultants or any other person) shall not, to the extent permitted by law, have any liability for the information contained herein or for any omissions arising therefrom or for any reliance that either party may place on such information. information. Plenisfer Investments SGR S.p.A. assumes no obligation to provide the recipient of this document with access to further information or to update or correct the information. Neither the receipt of such information by any person, nor the information contained in this document constitutes, or will be considered as constituting, the provision of investment advice by Plenisfer Investments SGR S.p.A. to such subjects. Under no circumstances should Plenisfer Investments SGR S.p.A. and its shareholders and subsidiaries or their employees be directly contacted in relation to this information.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

VAT n. & Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.