Marco Mencini, Head of Research Plenisfer Investments SGR

Copper recently hit record prices in a market characterised by significant volatility, influenced by a combination of geopolitical, economic, and supply and demand factors.

On the New York Commodity Exchange (COMEX, the main exchange for trading metal futures), prices hit an all-time high of $5.2255 per pound*[1] at the end of March, marking a 30% increase since the beginning of the year. On the London Metal Exchange (LME), copper surpassed the $10,000 per tonne mark in March, approaching all-time highs*.

Moreover, copper in the US is trading at a 17% premium to the London market, or a record premium of over $1300/tonne, compared to the historical delta of $50-100/tonne*.

This disparity reflects trade tensions, but above all expectations about possible tariffs: rumours about the imminent introduction of duties on copper imports by the Trump administration have fuelled speculation, prompting traders to increase stocks and contributing to the rise in prices.

Against this backdrop, smelters around the world are facing the combination of high copper prices and supply shortages: the result is squeezing margins and thus cutting production, which puts further pressure on the availability of copper, which is estimated to be in deficit by 200-400,000 tonnes annually (Source: Wood Mc Kenzie). This deficit is expected to continue even if a global slowdown occurs, due to the limited supply and the demand supported by the electrification and digitisation processes.

In summary, the copper market is currently being influenced by a combination of trade tensions, sector dynamics and speculation, with future prospects closely linked to the evolution of these factors. The uncertainty characterising the current scenario penalises copper producers, whose valuations do not fully reflect the price trend of the raw material. In particular, US players should benefit not only from a higher realisation price over time in light of the low investments made, but also from supportive policies in terms of financing, as the Trump administration is clearly focused on promoting US independence on strategic resources such as copper.

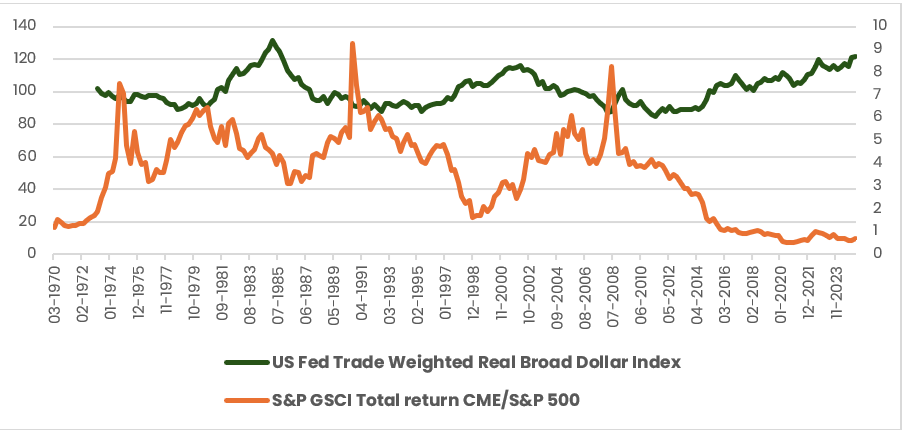

Moreover, the new US administration aims to solve the ‘twin deficit’ with austerity in government spending combined with lower interest rates and a weaker dollar. And in this scenario, durable assets tend to outperform US equities: today, commodities are trading at 50-year lows compared to US equities:

[1]* Source: Bloomberg

In light of the scenario and factors described, we expect, on the one hand, that the valuations of industry players may rise to match the new copper prices, and on the other hand, that these prices will remain subject to high volatility in the short term.

In our view, the copper price will remain supported by the imbalance between supply and demand. Indeed, it is worth remembering that the increased costs and time required to build new mines have raised the target price of copper needed to generate a return above the typical 15% rate: the target price is, in our view, currently $12/13,000 per tonne, which is still far from the current quotations. Only an increase in price will convince companies to start new projects, necessary to meet the growing demand for copper: but the price will have to rise structurally, as well as substantially, in order to incentivise supply or disincentivise demand, so that the market balances itself out.

The price is therefore the mechanism that can correct the current structural imbalance between supply and demand for copper: at Plenisfer we expect it to have cyclical ups and downs, but to rise in the long run to the target price of $12/13,000 per tonne and we therefore remain positive about the prospects for this strategic commodity.

Disclaimer

This analysis relates to Plenisfer Investments SGR S.p.A. (“Plenisfer Investments”) and is not a marketing communication relating to a Fund, investment product or investment services in your country. This document does not constitute an offer or invitation to sell or buy any securities or any business or enterprise described herein and does not form the basis of any contract.

Any opinions or forecasts provided are accurate as of the date specified, are subject to change without notice, do not predict future results and do not constitute a recommendation or offer of any investment product or service. Past performance does not predict future returns. There can be no assurance that an investment objective will be achieved or that there will be a return on capital. This analysis is addressed exclusively to professional investors in Italy pursuant to the Markets in Financial Instruments Directive 2014/65/EU (MiFID). It is not intended for retail investors or US Persons, as defined in Regulation S of the United States Securities Act of 1933, as amended.

The information is provided by Plenisfer Investments, authorized as a UCITS management company in Italy, regulated by the Bank of Italy - Via Niccolò Machiavelli 4, Trieste, 34132, Italy - CM: 15404 - LEI: 984500E9CB9BBCE3E272.

All data used in this analysis, unless otherwise indicated, is provided by Plenisfer Investments. This material and its contents may not be reproduced or distributed, in whole or in part, without the express written consent of Plenisfer Investments.

Plenisfer Investments SGR S.p.A.

Via Niccolò Machiavelli 4

34132 Trieste (TS)

Via Sant'Andrea 10/A, 20121 Milano (MI)

info@plenisfer.com

+39 02 0064 4000

Contact us at info@plenisfer.com

VAT n. & Tax ID: IT 01328320328

Belonging to Generali Italian VAT group: 01333550323

Registered to The National Compensation Fund

This is a marketing communication. Please refer to the Prospectus and Key Investor Information Document (KIID/KID) before making any final investment decisions. Past performance is no indication of future performance. Past performance is no indication of future performance.

The value of your investment and the return on it can go down as well as up and, on redemption, you may receive less than you originally invested.

© Copyright Plenisfer Investments onwards 2020. Designed by Creative Bulls. All rights reserved.